Breaking Down the Debt Cycle: Main Street Consumers and Credit Card Management

In an era of economic uncertainty, many Main Street consumers are leaning heavily on credit cards to manage day-to-day expenses. With inflation eating into disposable incomes, credit cards have become both a lifeline and a potential financial hazard. This article explores the trends in credit card usage among middle and lower-income consumers and provides actionable insights for businesses to offer sustainable payment solutions.

The Credit Card Conundrum

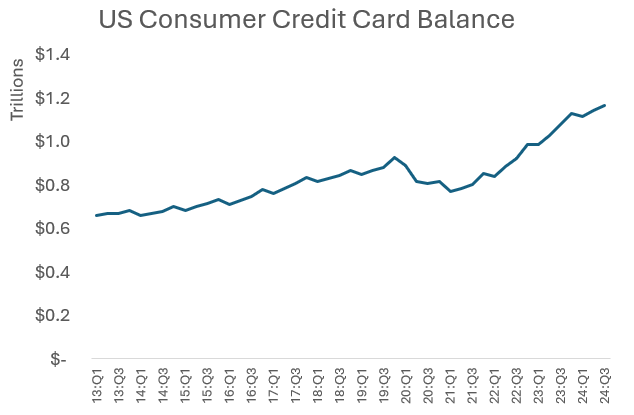

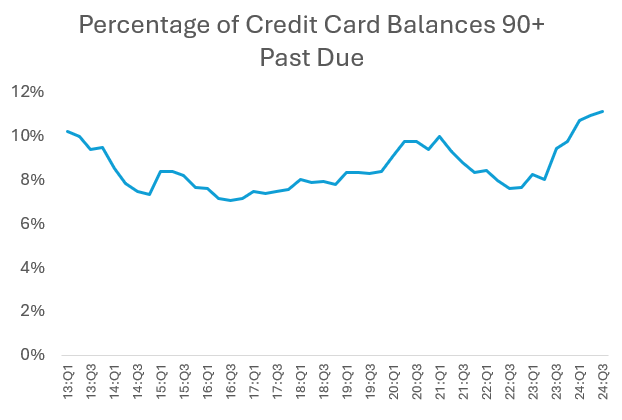

Trend: Credit card balances in the U.S. hit an all-time high of $1.03 trillion in 2024, according to the Federal Reserve Bank of New York. For Main Street consumers, this rise signals increasing reliance on credit to meet essential needs. The average credit card interest rate now hovers around 22%, exacerbating the financial strain on households already struggling with stretched budgets.

Analysis: For many families, credit cards are not merely tools for convenience but necessary means of survival. Groceries, gas, and utility bills often top the list of credit card charges, underscoring the squeeze on disposable incomes. As these balances grow, so does the challenge of repayment, creating a cycle of debt that becomes increasingly hard to escape.

Business Solutions: Rethinking Payment Plans

As credit card debt grows, businesses have an opportunity to step in with innovative payment solutions. Providing alternatives not only benefits consumers but also builds customer loyalty.

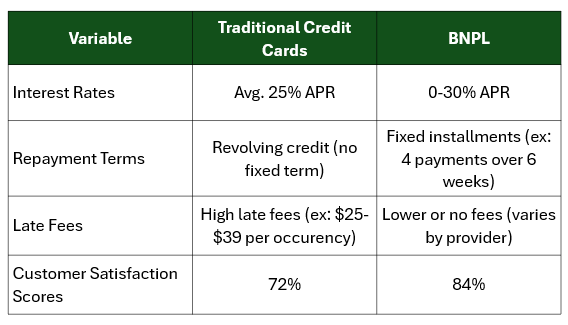

1. Installment Payment Plans: Options like "buy now, pay later" (BNPL) are gaining traction. Providers like Affirm and Klarna have shifted how consumers approach large or essential purchases. These plans offer fixed repayment schedules with transparent terms, making budgeting more manageable.

2. Subscription Models: Businesses can create subscription plans for essential goods and services, spreading costs over time. For example, meal kits, cleaning supplies, or even clothing rentals can be bundled into affordable monthly fees.

3. Reward Programs: Enhancing loyalty programs with cash-back incentives for timely payments can motivate consumers to stay on top of their bills while rewarding positive behaviors.

4. Flexible Billing Cycles: Adjusting billing cycles to align with customer paydays can help reduce missed payments and promote better financial health.

5. Financial Education Initiatives: Companies can partner with nonprofits or local organizations to provide financial literacy workshops, helping customers better manage their budgets and reduce reliance on high-interest credit.

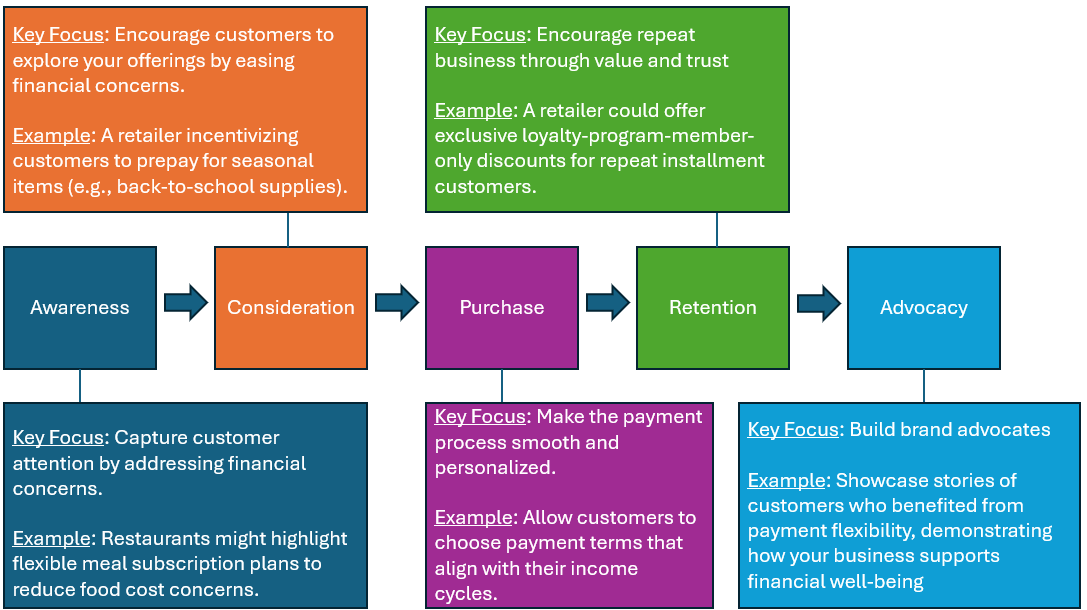

Strengthening Customer Relationships Through Financial Flexibility

Beyond offering alternative payment plans, businesses can foster stronger connections with their customers by aligning payment solutions with their financial realities. Here are some forward-thinking strategies:

- Dynamic Discounts: Offer discounts for upfront payments or early repayment of installment plans, incentivizing consumers to manage payments proactively.

- Data-Driven Insights: Utilize customer data to identify financial pain points and tailor payment solutions to their needs. For instance, if a significant portion of your customer base struggles with end-of-month expenses, introducing mid-month payment options can alleviate stress.

- Transparent Communication: Clearly communicate terms, fees, and repayment schedules to avoid customer confusion or mistrust. Transparency builds goodwill and long-term loyalty.

Looking Ahead: A Balanced Approach

Credit card debt will likely remain a part of the financial landscape for many Main Street consumers, but that doesn’t mean it has to be a barrier to financial health. Businesses have a unique role to play in reshaping how consumers manage their finances. By offering innovative payment solutions, promoting financial education, and building trust through transparency, businesses can position themselves as essential partners in their customers' economic recovery.

By understanding the financial struggles of their customer base and offering viable solutions, businesses can foster not only immediate sales but also lasting relationships.

Key Takeaways

- For Businesses: Offer installment plans, flexible billing cycles, rewards programs, and financial education initiatives to alleviate customer debt burdens and enhance loyalty.

- Customer-Centric Focus: Align payment options with consumer realities to build trust and drive long-term engagement.

By addressing the debt cycle collaboratively, businesses can drive growth while supporting financial stability for their customers.